Updates from Letty – December 9, 2016

Blog posts are the personal views of Letty Hardi and not official statements or records on behalf of the Falls Church City Council

Dear Friends,

As expected, it was a packed week full of City meetings and important topics – we had a lengthy joint work session with the School Board covering a spectrum of money matters, several economic development-related meetings and updates, and another GMHS campus working group meeting.

Whether you are a perennial budget watcher or want to learn, this is a good update for you. Fair warning – this can be a “eyes glazing over” blog post, but I tried to write it in an easy to understand way. I encourage you to set aside some time, grab a cup of tea, and read this update in between holiday parties and cookie baking this weekend. The financing options for GMHS/MEH are far more consequential than the annual budget debates, so as taxpayers – this is important, weighty stuff to understand and chime in with thoughts. While the FY18 budget won’t be voted on until next spring – we set the ball in motion this week and have several important votes next Monday as it relates to financial policies that will have implications for the coming budget. So we would like to hear from you! Monday at 730 pm is our final City Council meeting of 2016.

Read on, and as always – feel free to send me questions or feedback afterwards.

Best,

Letty

What Happened This Week:

City Council & School Board Joint Work Session

(1) Comprehensive Annual Financial Report (CAFR) – as we do each year, we reviewed the year end audit of our financial statements, conducted by our outside independent auditor. The FY16 CAFR is available online for review. It’s a lengthy, technical document that includes various accounting statements and reports, but pages iii to viii is a good “year in review”, including economic conditions and trends in the City and new and pipeline projects. Pages 4a to 4p is an overview of the City’s financial performance for FY16, including our revenues, expenditures, capital assets, and outstanding debt. The auditor’s report of summary begins on page 135. The TL;DR version is that there were no significant findings, other than one (for segregation of duties in both the general government and school offices) that has been identified in previous audits but difficult to remediate unless we increase staffing.

(2) GMHS Campus Affordability & Financial Modeling

The key affordability issues, as it relates to a new or renovated GMHS/MEH are: a) what can we legally afford, b) how much more can we afford with creative financing, and c) what are the risks and implications of trying to afford more? The full presentation is available online that attempts to answer those questions, but here’s my digested version:

- There are various caps, metrics, and policies currently in place that limit how much the City can borrow. Such include: debt service to total expenditures (12% cap), debt to assessed value (10% state law cap and 5% City cap), pay out ratios (how quickly is debt paid off), and debt per capita.

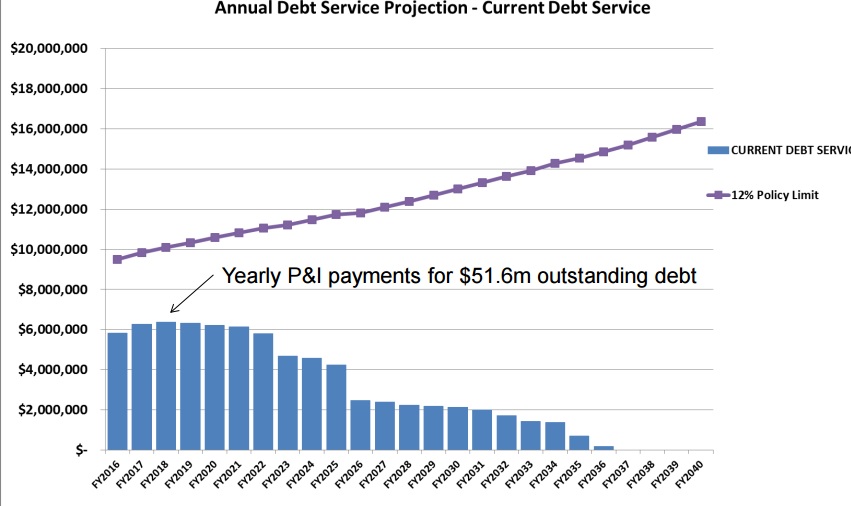

- Current debt service as it relates to 12% cap

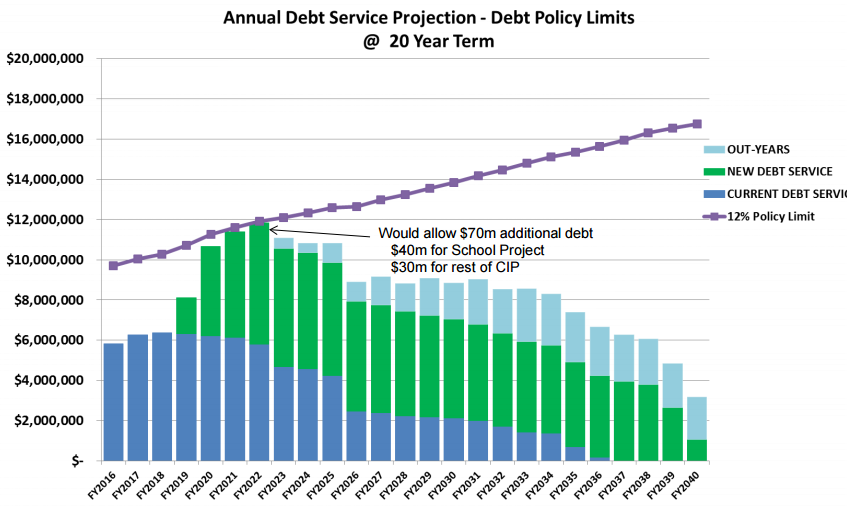

- How much can we afford? Under existing policy and without de-prioritizing other items in the adopted CIP, we can afford to borrow $40MM for the school project without hitting our policy cap. We have room for $70MM total in additional debt, but $30MM is already committed to other large capital projects such as the Library and City Hall.

- So – can we afford more, and if so – how? And how much will it cost the taxpayer? The most recent estimate for a new GMHS/expanded MEH campus is $114MM. Yes, we can afford $114MM and as currently modeled, it will cost 8-10 cents on the real estate tax rate (about $600 for the median homeowner), potentially some of it as soon as next year. There are many levers we have to pull in order to creatively finance this once in a generation expense as well as risks with taking on this level of debt. Here’s a summary of the levers and assumptions:

- Finance GMHS/MEH with 30 year debt. 20 year debt is what the City had traditionally used for capital projects. (30 vs 20 year debt is similar to a 30 year vs 15 year mortgage, where 15 years has more expensive monthly payments, but you pay less interest overall and pay off your mortgage sooner, while a 30 year mortgage makes a large expense more affordable.)

- Use capital reserves to pay for debt service. This would be a significant change in City financial management. Using reserves is analogous to using your savings account to pay for your monthly mortgage payment vs using your monthly income. We currently have $9MM in reserves, leftover from the water sale proceeds, and in this aggressive financing scenario, we would raise the real estate tax rate in advance (as early as this year) to bank the money in reserves to alleviate the burden during the highest years of debt service during the first 5 years.

- Commercially develop the 10 acres of land freed up by a smaller footprint of a new GMHS. Previous consultants had provided us a fairway estimate of $40MM for the 10 acres. The financing scenario assumes we could get 3 payments of $10MM each that would again go into capital reserves and be used to pay for debt service. Clearly there are risks with whether we would get the amount of $30-40MM and timing of those payments, all subject to economic conditions at the time – but also potential upside if the land is worth more.

- Use level debt financing. Level debt is similar to a traditional mortgage – payments are fixed and at the beginning of the loan, you’re paying off more interest at the beginning and less principal. Historically, the City has used level principal amortization – where we pay an equal principal amount throughout the life of the loan, so the debt service decreases over time as interest payments decline. It’s a more conservative way of municipal financing that reduces the overall cost of borrowing and protects future borrowing capacity.

- With taking on more risk, one recommendation is we would also need to bank more money in unassigned fund balance. Our current policy calls for 12-17% of expenses to be held in this “rainy day fund”. By taking on more debt, we risk a downgrade in credit rating, so our financial consultants recommend a 20% unassigned fund balance as mitigation. That would require $6MM more than what is in unassigned fund balance currently and would likely require a real estate tax increase to fund.

- Assumption: we assume property values grow at 2.5%, which is a reasonable expectation given past trends, but also upside/downside risk that is subject to economic conditions.

- Assumption: to limit the tax increases to 8-10 cents, we assume operational budgets are funded out of revenue growth – in other words, not requiring additional tax rate increases to fund annual government and school operations. With costs like health care and Metro that are largely out of our control and growing school population that puts pressure on the annual operating budget, this is a big assumption.

- Assumption: we’ve used 4% interest rate assumption in the financial modeling. Given the current political and economic climate, interest rates are currently expected to rise in the future.

- Assumption: this modeling is based on the currently adopted CIP, which does not include any new projects such as new elementary school options that may be needed when we reach capacity at Mt. Daniel (latest estimates of MD hitting the 660 enrollment cap, as committed to Fairfax County, is 2020).

- Assumption: positive tax revenues from commercial development of the 10 acres is not included in the modeling. This is a conservative approach. However, note that we wouldn’t be generating any revenue until a minimum of 2-3 years *after* the 10 acres is freed up when GMHS construction is complete, then sold/leased, and developed. If a November 2017 referendum happens, a new or renovated GMHS’s is targeted to be complete in 2021 so commercial tax revenue wouldn’t be realized until 2023 at the earliest.

- With a $114MM GMHS, we would be exceeding policy caps and the various metrics mentioned above. Slides 9-15 are useful comparisons of Falls Church vs neighboring jurisdictions. For example, our debt per capita would be the highest in Northern Virginia. https://fallschurch-va.granicus.com/MetaViewer.php?view_id=2&clip_id=786&meta_id=59057

- The small working group met this week and will convene again next week to take this data + the last several weeks worth of enrollment projections, costs, etc and prepare a set of options and pros/cons for discussion with both bodies in early January.

(3) Fiscal Policies Changes

In light of the financing challenge of the GMHS/MEH project and the rest of the ambitious CIP, we have been working on the changes to the fiscal policies. The proposed changes both build in flexibility to accommodate the financing levers discussed above and add more stringent policies to further strengthen the City’s financial position. The two key changes that will have implications for your tax rate:

- Increasing unassigned fund balance to 20%, should we borrow above our debt service 12% limit, mentioned above. This requires an injection of $6MM within 3 years.

- Funding a new “pay as you go” (ie, cash) capital maintenance target of $1 million per year, which represents 1% of our assets. This is intended to fund ongoing rehabilitation and replacement of existing buildings and heavy equipment and will reduce the current practice of relying on borrowing for these expenses.

Budget and Finance Chair Karen Oliver wrote a nice article that explains these policy changes and why they’re important here: https://www.fallschurchva.gov/Blog.aspx?IID=90#item. The policies will be up for a vote next Monday, December 12th.

(4) FY18 Preliminary Budget Forecast & Guidance – key headlines:

- Revenue growth for next budget year is predicted to be 3% which is about $2.4MM more than the current year. After taking out debt service and other costs, about $1.8MM is left for both general government and school budgets.

- Nearly 60% of revenues comes from real estate taxes. Of that, 22% is from commercial properties, 9% from apartments, and remainder 69% from residential properties.

- While we forecasted a high 12% sales tax growth for the FY17 budget due to new development projects like Harris Teeter, we return to a modest 3% sales tax growth in FY18 budget.

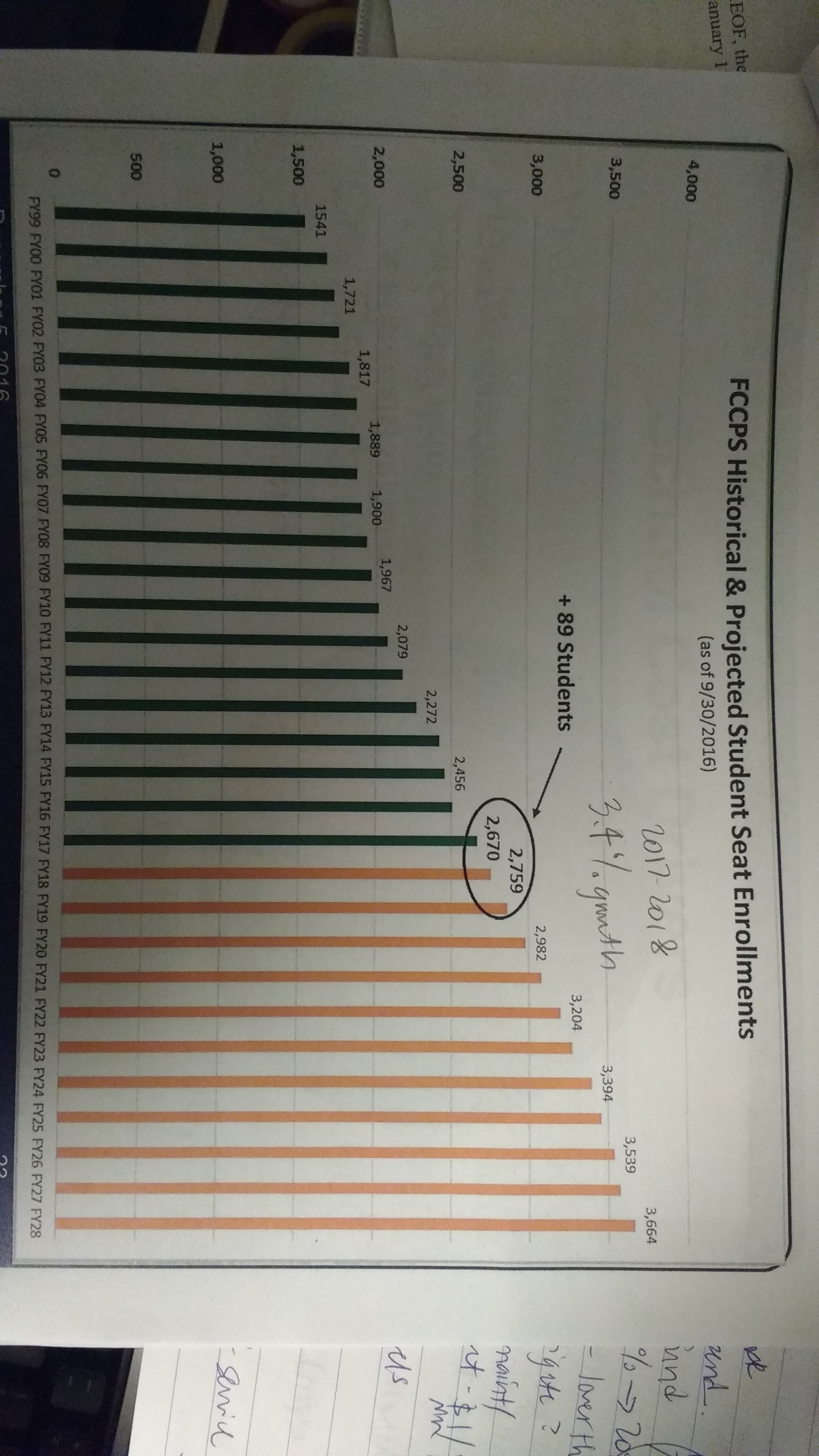

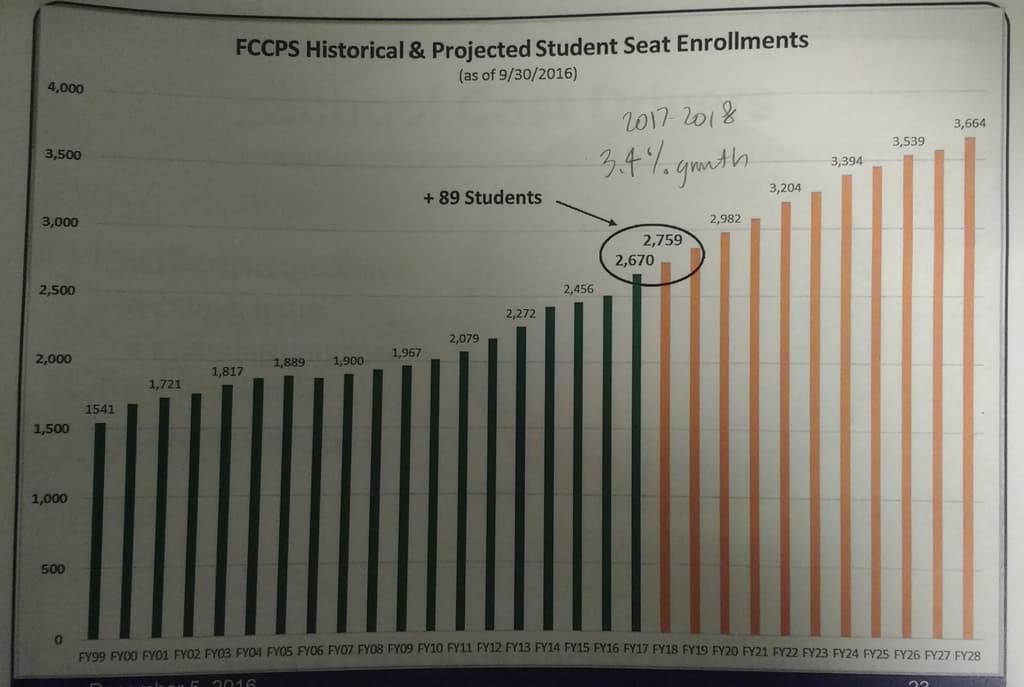

- There will be many pressures on the operating budget. Some early expenses discussed: WMATA contribution of $500-650K, over and above last year’s increase contribution to pay for programs like SafeTrack, decrease in fare revenues, and long term capital costs; increased retirement and health care contributions; funding student enrollment (predicted to be 3.4%), and of course – building reserves to pay for the GMHS financing scenario discussed above.

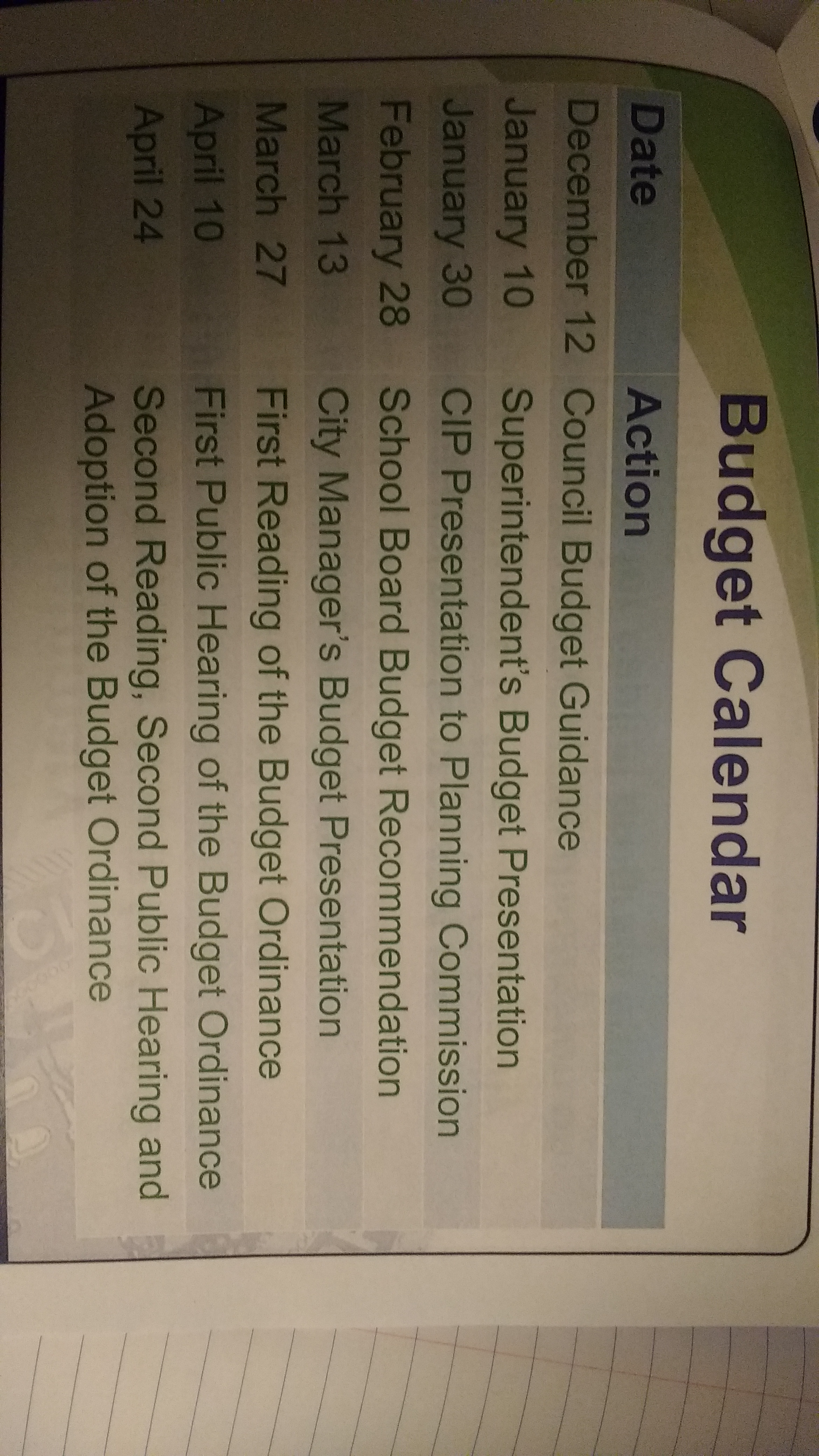

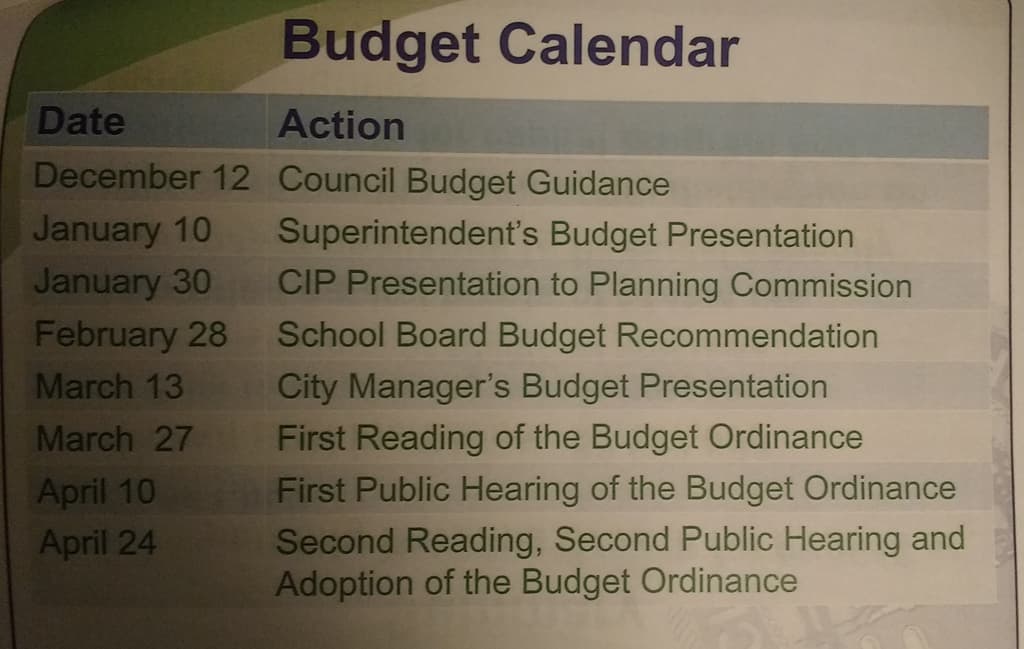

- Mark your calendars, here is the current calendar for the FY18 budget. The first date coming up is on next Monday, December 12th – City Council issues “budget guidance” to the City Manager, based on the early revenue and expenditures projections provided by the CFO this week. We discussed key themes for the budget guidance draft. More about Monday’s budget guidance in the “What’s Coming Up” section below.

Other Updates:

- The Planning Commission approved the site plans for a by-right development of a new Inns of Virginia hotel at 421 W. Broad, replacing the one currently there. Construction is expected to begin early next year with opening in 2018.

- The first review of Mason Row’s site plans by the Planning Commission will happen at their December 19th meeting. Expect a more detailed schedule with dates on other Boards and Commission meetings and a community meeting in January. Site plans have been uploaded online here: https://www.fallschurchva.gov/1381/Mason-Row-Broad-and-West-Streets and can also be viewed in paper form at City Hall.

What’s Coming Up:

- Mon, 12/12 – City Council meeting (last one of the year), 730 pm

We have a number of important topics on deck at next Monday’s meeting – including Budget Guidance, Changes to Fiscal Policies, approving the next phase of City Hall project. The agenda and supporting documents are uploaded for review.

In the Budget Guidance document, I wanted to highlight two important positions that were discussed in this week’s work session that’s in the proposed draft:

It is the Council’s intention to maintain appropriate discipline on operating budgets for General Governments and Schools with a vision toward reserving financial capacity for the major capital projects in the City’s immediate future, including the George Mason High School and Mary Ellen Henderson Middle School projects, the Mary Riley Styles Library project, and the City Hall Public Safety project. This reflects a concern about the capacity of tax payers to afford both operating budgets that exceed revenues from economic growth as well as future debt service for capital projects.

The Budget should provide options for funding improvements that will further the progress in making the City’s business districts vibrant, attractive, and walkable, and options for funding the neighborhood traffic calming program on a sustained basis.

- Thurs, 12/15 – Campus Working Group Meeting, 9 am (FCCPS Central Office)

- Superintendent Search Survey – if you missed the two community input meetings this week, you still have an opportunity to provide feedback on the qualities you’d like to see in the next superintendent of FCCPS. This is open to everyone in the community – not just current FCCPS families. Provide your feedback here: https://www.surveymonkey.com/r/9NHFVCT

- Calling all Accountants, Attorneys, Real Estate Professionals! Volunteers needed for the Board of Equalization (BOE)

- Tuesday, 1/3/17 – Joint City Council and School Board Work Session

- Monday, 1/16/17 – Save the Date! Martin Luther King Jr Day – we declared MLK Jr Day as a City-wide Day of Service and the City co-sponsored march at Tinner Hill. Stay tuned for various service opportunities and ways to contribute to the community in honor of Dr. King’s legacy.

- The Planning Commission approved the site plans for a by-right development of a new Inns of Virginia hotel at 421 W. Broad, replacing the one currently there. Construction is expected to begin early next year with opening in 2018.